3 Marketing Challenges Facing FinTech Brands

When Barclays launched the first ATM in 1967, no one imagined today’s financial ecosystem of mobile banking, blockchain, AI-based processes and digital currency. The global FinTech market has certainly matured since then, barreling toward $305.7 billion by 2023.

But according to Ritu Maryu, editor of Entrepreneur India, the industry’s growth is riddled with many peculiar problems. “I’ve not seen such kind of unique challenges in different sectors,” she remarked at the 2019 Web Summit.

While FinTech leaders navigate a fierce talent war, constantly evolving regulations and increasing security threats, their marketing departments are facing the downstream effects. Here are the top three:

Marketing to Young Buyer Personas

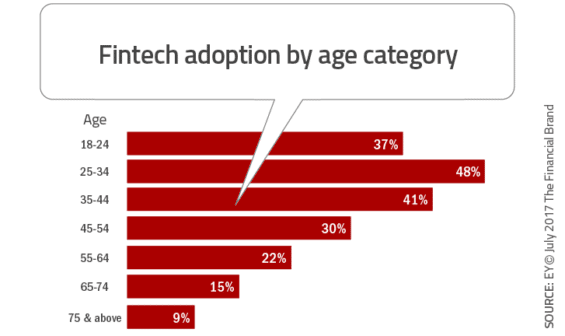

The digitally-native Millennial generation and the younger, mobile-first Gen Z are adopting financial technologies faster than older generations. For example, two-thirds of Millennials are putting more than 5% of their paychecks into savings, the highest savings rate of any current generation. And investment apps such as Betterment and Acorns are reaping the benefits.

In fact, Millennials love FinTech so much that a 2017 report found 33% believe they won’t need a bank at all in 5 years. As a result, B2C FinTech brands must market deep technology to a set of youthful buyer personas. This balancing act is exacerbated by the highly-regulated nature of financial communications. FinTech brands that are successfully marketing to Millennials are embracing:

Personalization. Selligent found that 74% of global consumers expect financial brands to treat them as individuals. Personalization should transcend all marcomm – from email marketing to social customer service.

Brand Awareness. EY’s 2016 FinTech Adoption Index discovered that over 50% of consumers say the biggest reason they don’t use FinTech products is due to lack of awareness that a product even exists. Therefore, brands should invest strongly in a PR program to break through the increasingly cluttered market.

Cross-Selling. CapGemini’s 2017 World Retail Banking Report uncovered that Millennials are highly likely to buy additional products from their current FinTech providers. That means customer nurturing and success activities are just as important as brand awareness.

Reaching an Expanding Pool of FinTech Press

As adoption of financial technologies has increased, so have the number of media outlets that cover them. Over the past year, dozens of FinTech-focused trade media sites, podcasts and newsletters have launched, like Cheddar’s “Crypto Craze.” In addition, authoritative publications, such as CNBC and Financial Times, have hired beat writers to pump out stories on mobile payments, cryptocurrency, etc.

More media outlets equate to more opportunities to tell brand stories, and that’s good, right? Yes, but it also adds to the noisy, cluttered marketplace, requiring more muscle and strategy by FinTech PR firms.

The Need for Cybersecurity Messaging

For every high-profile financial breach, like the recent Capital One hack, there are dozens of more cybersecurity vulnerabilities and incidents. In fact, Accenture says FinServ takes in the highest cost from cybercrime at an average of $18.3 million per company.

As a result, FinTech brands - from startups to enterprise - must have a multi-layered security communications strategy that includes external and internal messaging, a crisis response plan, and even security thought leadership positioning.

FinTech companies looking to increase their market share and mindshare need a PR firm that understands their industry, the technologies that their products are built on, as well as their buyer personas. Download Alloy’s whitepaper, Rethinking the RFP Process: How to Select a Tech PR Partner to Push the Limits to get started.

:quality(80))

:quality(80))

:quality(80))

:quality(80))

:quality(80))

:quality(80))

:quality(80))

:quality(80))

:quality(80))

:quality(80))